Gear up for a super future!

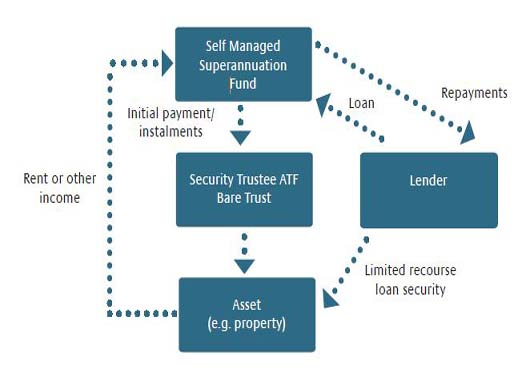

Figure 1

John Manuel

Prosperity Advisers Group

Superannuation is an attractive investment tool for retirement. Significant tax incentives within the superannuation environment mean investors can accumulate wealth more effectively within super than they could by investing in an identical property outside of super.

Tax advantages of Super

• Maximum income tax rate of 15% and Capital Gains Tax discounted rate of 10% whilst fund is in accumulation phase.

• Zero income and Capital Gains Tax whilst fund is in pension phase, and zero tax on withdrawals where a member is over 60 years of age.

• 100% tax reduction at your full marginal tax rate on concessional contributions to super (via salary sacrifice).

• Where investment is in property, tax deductions are available in the super fund for interest and property holding costs which may reduce the 15% superannuation contribution tax to nil.

More tax effective than ‘negative gearing’

Up until now the tax effective use of gearing strategy has been based on the benefit of tax deductible interest payments, and other related costs outweighing income in the short term, with the expectation of a future capital gain taxed at a concessional rate.

This is the underlying basis of the traditional ‘negatively geared’ rental property.

In a negative gearing scenario, the tax benefit is only derived from the tax deduction of interest and other related costs, whereas any payments directed towards the actual purchase price of the investment do not contribute towards an immediate tax benefit.

With a Super Gearing strategy, a personal tax reduction (via a salary sacrifice) will be triggered upon the contribution of funds into super, effectively providing a deduction for payments towards the purchase price of your investment with the related interest and holding costs acting to offset any contributions tax payable by the super fund.

Limited recourse borrowing arrangements – the structure

In order to comply with the strict borrowing regulations set out in the Superannuation Industry (Supervision) Act 1993 (SIS Act), a particular legal structure is required to be established (structure to be delivered in a simple and practical form). A complete outline of the required structure is set in figure 1.

This structure utilises an exception to the borrowing restrictions set out in section 67(4A) of the SIS Act, which state that a superannuation fund trustee may borrow to acquire a beneficial interest in an asset which is held in trust for it.

Upon purchase of a geared investment, the Security Trustee is the legal owner of the asset, however the beneficial interest is held by the superannuation fund which will make instalment payments to acquire the asset over time.

A critical requirement of the structure is that the loan facility is limited to recourse over the asset (ie single investment property) of the Bare Trust, and therefore other super fund assets are not utilised as security. Whilst an overall legal arrangement exists, the practical application and use of the structure remains simple.

There is much speculation that the May Federal Budget could put an end to Super Gearing in the future. Accordingly there may be limited time to act.

For further information contact Prosperity Advisers Group on (02) 4907 7222, email mail@prosperityadvisers.com.au or visit www.prosperityadvisers.com.au

John Manuel

John Manuel

is Director, Financial Services at Prosperity Advisers Group.

John joined the firm in 1998 as a Senior Accountant and became a Prosperity Director in January 2004. John is both a Chartered Accountant and Financial Planner with the Institute of Chartered Accountants recognising him with a Financial Planning Specialist designation.

Other Articles from this issue

Larger premises for Fitness Junction

After 15 years in the same location Fitness Junction has moved to larger premises just around the corner at 224 Union S...

Focus required on affordable homes

A new focus on the provision of smaller, more affordable properties is urgently required to meet the needs of thousands ...

ME Program provides students with commercial acumen

The Department of Defence funded ME Program is providing students from partner school, St Philips Christian College, wit...